Finance App With Secure Expense And Savings Management

A finance app can help users manage daily expenses, monthly budgets, savings goals, repayments, and short-term money needs in one place. Many people struggle to track where their income goes each month because expenses are spread across bills, groceries, rent, travel, shopping, subscriptions, EMIs, and emergency costs. A finance app can make this process easier by helping users monitor payments, plan budgets, and review financial activity more clearly.

When users need to borrow, financial planning becomes even more important. A loan calculator can help estimate EMI before applying for any loan, allowing borrowers to check whether repayment fits their income. Digital payment options such as upi can also support easier repayments when available. However, a finance app should not only be used for payments or borrowing. It should help users make better decisions about spending, saving, and repayment.

Online Loan Apply and Digital Finance Planning

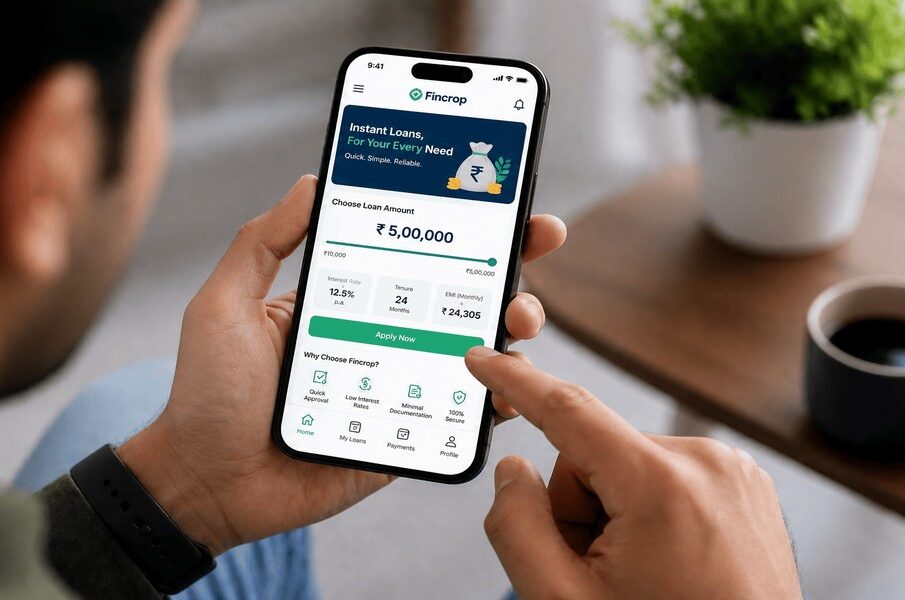

Online Loan Apply can be useful when users need financial support for urgent or planned expenses. Through Online Loan Apply, borrowers may be able to submit loan applications digitally, upload documents, check eligibility, estimate EMI, and track the application status without depending completely on offline paperwork.

Online Loan Apply should always begin with budget review. Before submitting any application, users should check their income, fixed expenses, existing EMIs, savings, and emergency needs. A loan may provide quick support, but repayment will continue every month. This is why users should calculate EMI before choosing any loan amount.

A finance app can support Online Loan Apply decisions by helping users understand whether a new EMI can fit their monthly budget. Online Loan Apply is useful only when the borrower understands the repayment terms, interest rate, fees, tenure, and total cost. Instead of applying quickly, users should first use a loan calculator and check affordability.

What Is a Finance App?

A finance app is a digital tool that helps users manage money-related activities. It may help track expenses, organize payments, monitor savings, review budgets, manage due dates, and record financial transactions. Some users may also use it to understand spending patterns and improve monthly financial discipline.

The main purpose of a finance app is to give users better visibility over money movement. When income and expenses are tracked regularly, it becomes easier to identify unnecessary spending and plan savings. Users can also understand whether they have enough room in their budget for a new EMI.

A finance app is useful for salaried individuals, self-employed users, students, families, and small business owners. Anyone who wants to manage money more clearly can benefit from structured tracking and planning.

Why Expense Tracking Matters

Expense tracking is one of the most important parts of personal finance. Many users know their monthly income but do not know exactly how much they spend on different categories. Small expenses may look harmless individually, but they can become a large amount by the end of the month.

A finance app can help users track recurring payments, daily purchases, utility bills, digital transfers, and EMI obligations. This allows users to understand where money is being spent and where costs can be reduced.

Expense tracking also helps users avoid unnecessary borrowing. If users can identify avoidable spending, they may be able to handle some expenses without taking a loan. When borrowing is necessary, expense tracking helps users decide a safe EMI amount.

How a Loan Calculator Supports Better Planning

A loan calculator helps users estimate monthly EMI before applying for a loan. It usually requires the loan amount, interest rate, and repayment tenure. Based on these details, it shows the expected EMI amount.

This is useful because borrowers can compare different repayment options before making a decision. A longer tenure may reduce monthly EMI but can increase total interest cost. A shorter tenure may reduce overall interest but can increase monthly repayment pressure.

When used along with a finance app, a loan calculator can help users understand how a new EMI will affect their monthly budget. Instead of applying without clarity, users can check whether repayment will disturb essential expenses such as rent, groceries, school fees, bills, or savings.

Savings Management Through a Finance App

Savings management is another important benefit of using a finance app. Users can set monthly savings goals, track progress, and reduce unnecessary expenses. This helps build financial stability over time.

A good savings habit can reduce dependency on loans for every unexpected expense. Even a small emergency fund can help users manage medical needs, repairs, travel, or urgent bills without immediate borrowing.

A finance app can also help users separate essential savings from flexible spending. When savings are planned at the beginning of the month, users are less likely to spend everything before the month ends. This supports better long-term financial health.

Budgeting for Monthly Stability

Budgeting helps users decide how income should be divided across expenses, savings, repayments, and personal spending. Without a budget, money may be spent without clear control, leading to cash shortages before the next income cycle.

A finance app can help users prepare a monthly budget by showing spending categories. Users can check how much they spend on food, travel, bills, shopping, subscriptions, and loan repayments. This makes it easier to adjust spending when needed.

A balanced budget should include room for savings and emergencies. Users should avoid creating a budget where every rupee is already committed to expenses. Financial flexibility is important, especially when unexpected costs arise.

When Borrowing May Be Needed

Borrowing may be useful when users face genuine expenses that cannot be delayed. These may include medical bills, urgent repairs, education fees, rent gaps, or temporary income delays. In such situations, a loan can provide short-term support if repayment is manageable.

However, borrowing should not be used for unnecessary purchases or impulse spending. A finance app can help users check whether the expense is important and whether the loan EMI can be handled.

Before borrowing, users should compare the loan amount, interest rate, tenure, fees, repayment date, and total repayment cost. A loan should solve a financial need without creating repayment stress.

Role of Upi in Daily Finance Management

Upi has made digital payments easier for many users. It can be used for transfers, bills, purchases, and loan repayments where supported. Since payments happen quickly, users should track them carefully to avoid overspending.

A finance app can help users review upi transactions and understand spending behaviour. This is important because easy payments can sometimes lead to frequent small expenses that are not noticed immediately.

For loan repayment, upi can be useful when accepted by the platform. Borrowers may be able to pay EMIs or dues directly from their bank account. Users should always verify payment details and keep transaction confirmations for future reference.

Common Finance Mistakes to Avoid

One common mistake is not reviewing expenses regularly. Users may track spending for a few days and then stop. Consistent tracking is necessary to understand financial habits.

Another mistake is borrowing without calculating EMI. A loan calculator should be used before applying so users know the repayment amount in advance.

Some users also ignore due dates. Missed bill payments or EMI delays can lead to penalties and financial stress. Setting reminders through a finance app can help avoid this issue.

Another mistake is not maintaining emergency savings. Without savings, users may need to borrow for every sudden expense. A small monthly contribution can help build a useful safety fund over time.

How a Finance App Helps With Repayment Discipline

Repayment discipline is important for anyone who has borrowed money. A finance app can help users track EMI due dates, payment history, and monthly repayment obligations. This reduces the risk of missed payments.

Users can also plan their monthly cash flow better. If an EMI is due on a specific date, they can make sure enough balance is available before that date. This helps avoid late fees and repayment stress.

A finance app can also show how much of the monthly income is going toward repayments. If this amount becomes too high, users should avoid taking additional loans until existing obligations reduce.

Loan App Before the Final Decision

A loan app can help users apply digitally, check eligibility, upload documents, estimate EMI, and track application status. However, a loan app should be used only after reviewing the monthly budget properly. Fast access to credit should not replace careful planning.

Before using a loan app, users should check whether the loan is truly needed. If the expense can be managed through savings or delayed payment, borrowing may not be necessary. If the loan is required, the amount should be limited to the actual need.

A loan app can support convenience, but users must check interest rate, EMI, tenure, fees, repayment date, and late payment charges. A loan app is most useful when it helps borrowers make informed decisions. Before accepting any offer through a loan app, users should calculate EMI, review terms, and ensure repayment is affordable.

Conclusion

A finance app can help users manage expenses, savings, repayments, and monthly budgets with better clarity. It can support financial discipline by helping users track spending, plan savings, monitor due dates, and review repayment capacity. When borrowing is necessary, users should plan carefully before applying.

A loan calculator helps estimate EMI and compare repayment options before taking a loan. Digital payment methods such as upi can make payments and repayments easier when used responsibly. Whether users consider Online Loan Apply or use a loan app for borrowing, the focus should remain on affordability, clear terms, and timely repayment. A finance app works best when it supports better money management instead of impulsive financial decisions.

FAQs

What is a finance app?

A finance app is a digital tool that helps users track expenses, manage budgets, monitor savings, review payments, and plan financial activities more clearly.

How does Online Loan Apply work?

Online Loan Apply allows users to submit loan applications digitally, upload documents, check eligibility, estimate EMI, and track the application status online.

Why should I use a loan calculator before borrowing?

A loan calculator helps estimate monthly EMI based on loan amount, interest rate, and tenure. It helps users check whether repayment fits their budget.

Can upi help with loan repayment?

Yes, some loan platforms may support upi for EMI repayment or due payments. Users should confirm accepted repayment methods before making a payment.

How does a loan app help borrowers?

A loan app can help users apply for loans digitally, upload documents, check EMI estimates, review loan details, and track application status.

Why is expense tracking important?

Expense tracking helps users understand spending patterns, reduce unnecessary costs, plan savings, and avoid borrowing without proper need.

What should I check before applying for a loan?

Users should check interest rate, EMI, tenure, processing fee, repayment date, late payment charges, total repayment amount, and payment options.

What mistakes should I avoid while using a finance app?

Avoid irregular expense tracking, ignoring repayment reminders, borrowing without EMI calculation, overspending through digital payments, and skipping savings planning.

-

Mortgage Advice Cardiff: Why Use a Buy-to-Let Mortgage Broker Instead of Going Direct

If you’re thinking of investing in a buy-to-let property, one of the ... -

-

-

-